We’ve put together a spring round-up for our clients, here’s what you need to know about the latest Tax and accounting topics this spring.

MTD for VAT is Compulsory

If you’re not already submitting your VAT returns using MTD-enabled software, you need to take action now. You will need to sign-up for MTD if you haven’t already, and you will need to ensure you’re using MTD-compliant software to submit your digital VAT returns.

For VAT periods starting on and after 1 April 2022 all VAT records must be recorded digitally and returns must be submitted under the Making Tax Digital (MTD) regime.

If you are not already submitting your VAT returns using MTD-enabled software (or asking us to do so) you need to take action. Recording your VAT transactions using a spreadsheet is acceptable under MTD – however you will need software to transmit the VAT data to HMRC without retyping or copy/pasting the figures. There is plenty of choice in the market, from cloud-based systems to relatively simple bridging software that will connect to your spreadsheets. Our team can advise you on the best solutions for your particular circumstances, so please get in touch. You can also see our recommended solutions on our Cloud Bookkeeping page here.

Please take action as soon as possible – penalties for submitting your return digitally are set at £400. If your turnover is relatively low, it may be worth discussing de-registering for VAT with your accountant.

Declare Your Covid-19 Grants

The Covid-19 support grants (CJRS, SEISS and Eat Out to Help Out) are taxable and should be declared on your business’ tax return. For Corporation Tax (CT) you must report amounts received in the accounting period covered by the return, not grants claimed for the period and paid in a later period.

The first CJRS grants were paid in April 2020 but the CT return forms were not amended to include special boxes to report those grants until September 2021. If your CT return was submitted before the new version of the form was released the grant figures will not be easy to spot. If HMRC cannot match the reported CJRS grant on the CT return to the amount paid to the company it will write to request an explanation. If you receive such a letter please talk to us as soon as possible. It is important to take the letter seriously and reply with 30 days, as failure to do so may trigger a formal tax enquiry into your business.

We will either amend the CT return to include any omitted Covid-19 grant income or confirm to HMRC that all grant income has

been included within reported income.

VAT on Termination Fees

Contract termination fees can be a bitter pill to swallow when you just want out of an expensive agreement. What’s worse is that some suppliers will charge VAT on top of the cancellation fee while others will not.

The law has been a bit of a mess but HMRC has laid down firm guidance on how termination fees should be treated for VAT purposes from 1 April 2022. From this date any fee paid on the early termination of a contract should follow the VAT treatment of the main supply under that contract.

Where your business charges cancellation fees, say for gym membership, hiring of rooms or restaurant tables, you need to review your VAT policy to ensure that it is in line with the new HMRC guidance from 1 April. We can help you with this.

If you are planning to terminate a contract early, which would create a cancellation fee, consider doing this before 1 April 2022. But first ask your supplier about the level of the charges and whether they intend to charge VAT on top.

Covid-19 Sick Pay Scheme Ends

As we are now at the ‘living with Covid-19’ stage of the pandemic the Government has decided to close the Covid-19- related statutory sick pay (SSP) rebate scheme on 17 March 2022.

The scheme re-opened on 21st Dec 2021 for employers with fewer than 250 employees. It permits the employer to reclaim up to 14 days of SSP paid to an employee who is unwell or isolating due to Covid-19 and allows SSP to be paid from the first (rather than 4th) day of sick leave.

All claims for refunds of SSP paid must be submitted to HMRC by 24th March 2022. This is also the deadline for amending any earlier SSP refund claims.

This is an incredibly tight deadline, especially as the SSP has to be paid to the employee before it can be reclaimed. We can help you with your SSP refund claims.

Also from 25th March 2022, SSP will revert to being payable from the fourth day of absence from work, even if the absence is due to Covid-19.

Tax on PPI Interest

Do you remember those annoying ‘claim back your PPI’ adverts? Thousands of people received repayments, which included interest calculated at 8% on the PPI premiums refunded.

Where the PPI settlement was paid after September 2013 the bank or insurance company should have deducted tax at 20% from the interest element. This was correct but if the interest received is covered by the taxpayer’s savings allowance of £1,000 or £500 that tax can be reclaimed.

This is turning into another potential scam as ‘tax refund companies’ are persuading taxpayers to submit refund claims for the tax deducted and some keep a large slice of the refund. HMRC is also getting overwhelmed with claims.

If you received a PPI settlement, the interest element and tax deducted should have been declared on your self assessment tax return for the year in which you received the money. We can help you amend your earlier tax return to declare any PPI interest and claim a tax refund.

If you are not within the self assessment system you need to claim the tax refund on a form R40. This can be done online by signing in through Government Gateway or by post, but an online claim will be processed quicker. Do not under any circumstances let anyone else use your Government Gateway credentials to claim a tax refund on your behalf.

Hospitality VAT Rates Increase

If you operate in these sectors, check that your accounting system will apply the correct VAT rate.

The hospitality and through the Covid-19 reduced amount of VAT tourist sectors pandemic by to HMRC in have been supported being able to pay a respect of most sales. The reduced VAT rate was 5% from 15 July 2020 to 30 September 2021 and 12.5% from 1 October 2021 to 31 March 2022.

The sales affected by this special reduced VAT rate include: restaurant meals, hot takeaway meals (not sandwiches), hotel and similar accommodation, and entrance fees to tourist attractions. The reduced VAT rate also applied to non-alcoholic drinks taken with a restaurant or café mean eaten in-house, but where the drink was part of a takeaway it had to be hot.

The business was not required to lower its prices to reflect the reduced VAT so could keep the difference as extra profit. But that benefit is now ending as the standard rate of 20% is restored from 1st April 2022.

If you operate in these sectors you should check that your accounting system and point of sale equipment will apply the correct VAT rate from 1 April 2022. You also need to be particularly careful with the VAT return for the period that straddles 1 April. We can double-check the figures for you before submitting the return.

It may be a good idea to review all VAT returns covering the reduced-rate periods to see if you have overpaid or underpaid VAT. Any such small errors can be adjusted on your next VAT return.

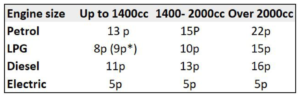

Advisory Fuel Rates

The price of road fuel has increased significantly in the last few months and HMRC has responded by raising all the advisory fuel mileage rates for company cars from 1 December 2021.

If you pay for the fuel in your company car your employer can reimburse you for the cost of business journeys in that car at the following mileage rates tax free:

*The LPG mileage rate for the smallest cars was reduced from 1 March 2022.

As diesel engines tend to be bigger, the division between rates is set at 1600cc rather than 1400cc.

Cryptoassets Are Taxable

In uncertain times people instinctively look for alternative ways to invest and some may choose cryptoassets such as Bitcoin and non-fungible tokens.

If you decide to go digital with your investments, think about how the profit or loss you make on these assets will be taxed. HMRC does not consider cryptoassets, such as Bitcoin, to be a form of money or currency, so the special tax rules that apply to holding and lending money do not apply to cryptoassets.

Where cryptoassets are lent or ‘staked’ (lent to a platform which lends on to various borrowers) the return provided to the asset owner is not ‘interest’ but is taxable either as sundry income or a capital gain.

HMRC is unlikely to consider transactions in cryptoassets as trading, so by default the transactions are capital and any profits must be taxed as capital gains. This means that for every sale or exchange of cryptoassets a gain or loss must be calculated.

This can create serious practical problems as crypto- transactions are often automated and carried out in vast numbers over short periods. You need to extract the necessary transaction data from the digital exchanges and digital wallets you use so that each transaction can be analysed into a capital gains tax computation. We are not aware of any software that will do this yet so this information gathering can be time consuming and expensive.

Finally, HMRC is aware of cryptoasset transactions as it receives information about customers from digital exchanges.

Valuation of Let Property

When an individual dies everything they own is valued to calculate the Inheritance Tax (IHT) due on their estate. These assets include the deceased’s main home and any let properties they may own.

All of the assets must be valued based on a deemed transfer at open market value immediately before the deceased’s death. It is the condition of the assets as they existed at the date of death that is important, not the value at some later date after any pre-sale adjustments have been made.

Where a let property has a tenant in occupation at the date of death the value of that property for IHT purposes is the tenanted value – how much the property could be sold for with the tenant in residence – not the ‘with vacant possession’ value. This value should also take account of the unexpired period on the lease or licence at the date of death, as a longer outstanding lease period will generate a higher discount on the vacant possession value than a shorter lease term.

Where the property is jointly owned, only the proportion of the value attributable to the deceased should be included in the estate. It is crucial to find out whether the property is owned as joint tenants (‘joint owners’ in Scotland) or as tenants in common (‘common ownership’ in Scotland). The executors also need to know the relationship between any joint tenants as this determines the valuation method.

We can help you with the IHT forms at this difficult time, so please get in touch.

Interest on Late Paid Tax

All late paid tax now carries interest at 3%. Where the tax has been outstanding for more than six months a 5% surcharge on the outstanding amount may also apply.

Surcharge rates of up to 15% can apply for VAT paid just one day late. If you can only pay some of your tax bills it often makes sense to prioritise the VAT but we can help you decide.

A first step when faced with a tax bill you cannot pay should be to contact HMRC and make an arrangement to spread the bill over a number of months. This is called a Time to Pay agreement and can be done online if you owe HMRC less than £30,000. Where the debt is greater than £30,000 or you need more than a year to pay, you need to speak to an HMRC officer and provide more information. We can help you with that.

If you have income tax still outstanding from 2019- 20 but you are due a tax repayment for 2020-21 you might assume that the repayment would be off-set against the tax due and prevent any further interest running. Unfortunately this is not how the tax rules work. The tax repayment for 2020-21 is generally off-set against the outstanding tax, but only with effect from the final deadline for submitting the tax return: 31 January 2022 for the 2020-21 tax return.

If your 2020-21 tax return was submitted earlier than 31 January 2022 we can ask that HMRC treats the effective date of the repayment off-set as the date when your tax return was logged as received by HMRC. This should remove much of the interest charged.